Now Live:

SearchCompliances in India, Outsource ComplianceCA Siddhartha AgrawalApr 6, 20204 min readUpdated: Nov 12, 2025

Once an investor sets-up a business in India, whether it is a liaison office, project office, branch or company, that business needs to comply with Indian regulations. In this note we will discuss the recurring compliances that affect day to day business. Within each compliance activity

All businesses in India need to maintain accounting records that meet the Indian Generally Accepted Accounting Policies. A business entity is free to decide their accounting year as financial, calendar or otherwise to match their global reporting norms. However, under the Indian income tax laws it is mandatory to close the books of accounts on a financial year basis i.e. April 1 to March 31.

Businesses need to draft appropriate employment contracts keeping

in view the income tax laws and employment regulations. In terms of compliance, they are required to pay monthly salary, generate pay slips and ensure regulatory compliances under labour laws. Furthermore, salaries are structured at the time of set-up, revision or when there is

Under the Indian Companies Act it is mandatory for businesses to have their accounts audited by an Indian firm of chartered accountants. These audited accounts are to be filed with the Registrar of companies (‘ROC’) and, in some cases, with the Reserve Bank of India.

Businesses with an annual turnover exceeding INR 10 million (USD 150,000 approx) need to additionally have accounts audited under specific provisions of the Indian income tax laws and certified by an Indian firm of chartered accountants.

Private Companies exceeding a turnover INR 2 billion (USD 31millions approx) or outstanding borrowings of INR 1 billion (USD 15 million approx), need to have an internal audit system in place, either outsourced to an Indian firm of chartered accountants or through their in-house team, the latter being prevalant in case of large corporates.

Businesses need to determine their annual tax payment and ensure its deposit under an instalment plan commonly referred to as Advance Tax. Delays, deferment or incorrect calculations attract penal provisions. At the year end, an annual return together with audited accounts and tax audit report must be submitted e.g. in case of Financial Year 2020-21, advance taxes have to be deposited by June 15 (15%), September 15 (45%), December 15th (75%) and March 15 (100%). The Annual Return

for this year is to be submitted by September 30, 2020 / November 30, 2020.

Businesses having cross border dealings with related concerns fall within ambit of Indian Transfer Pricing regulations. This requires the maintenance of documentation and certification by an Indian firm of chartered accountants confirming that the firm’s dealings with related concern were at an arm’s length, and the profits were appropriately reported by the Indian business entity.

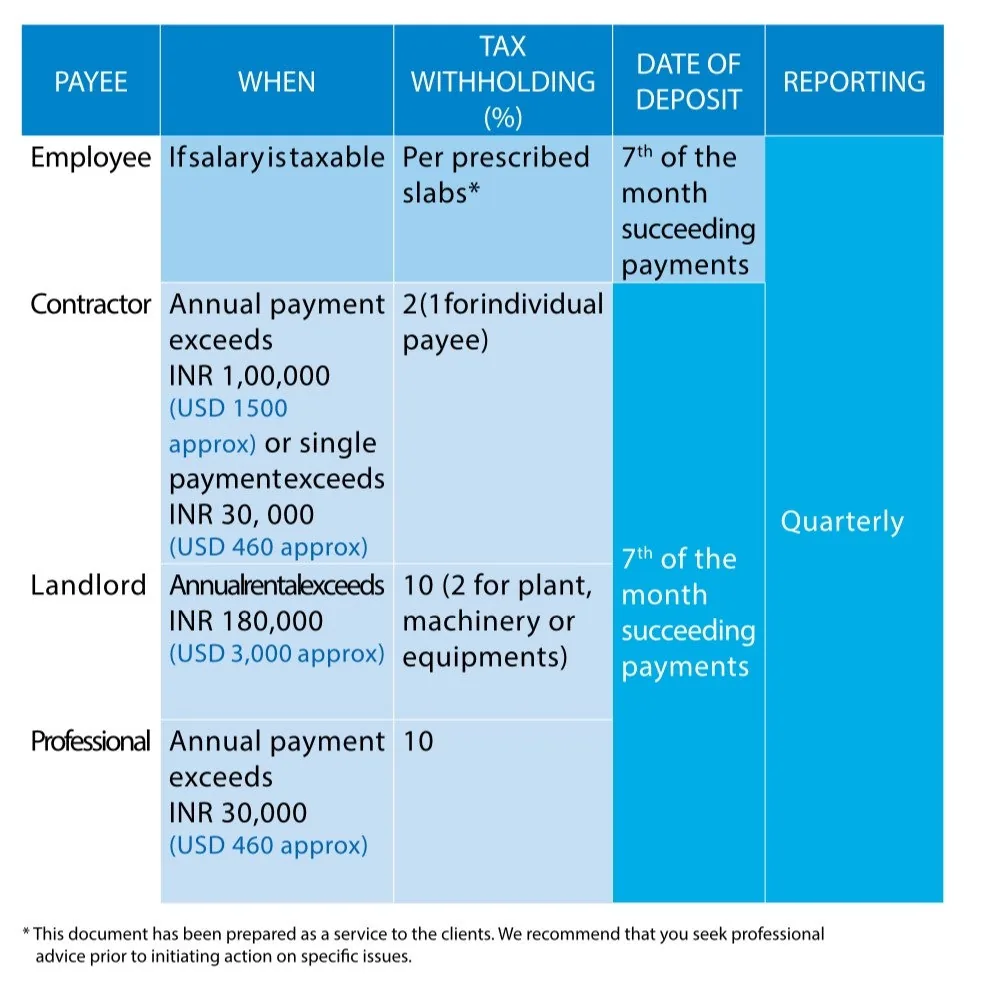

Businesses need to withhold tax on specified payments viz salary, contractual, etc.

An expatriate deputed to India is liable to tax in respect of his remuneration. The components of taxable remuneration are similar to those applicable to a local employee, though one may explore relief under the Double Tax Avoidance Agreement between India and the parent country. The expatriate would need to file an annual personal tax return with the Indian tax authorities by July 31st. All foreign nationals who are likely to exceed 180 days stay in India, need to register within 14 days of their arrival with the Foreigners Regional Registraion Office.

Businesses engaged in cross border trading need to comply with customs duty regulations. The duty varies between products. The compliance requirement includes determination and deposit of duty prior to clearance of goods by the customs authority . While basic customs duty remains, the Counter Vailing Duty (CVD) and Special Additional Duty (SAD) of customs is included in GST.

GST is applicable on supply of goods and/or services. It consolidates

the erstwhile excise duty, service tax, central and local VAT, amongst others. Compliances include deposit of taxes and filing of monthly returns.

Businesses in India need to comply with secretarial matters specified under the Indian Companies Act and report to the concerned ROC.

An employer needs to consider the impact of Provident Fund, government regulated Pension Plan scheme. Furthermore, an outgoing employee, who has exceeded 5 years of service, is to be paid Gratuity calculated as per specified scales.

Industrial units are covered by the Employee State Insurance, Industrial Dispute Act, Contract Labour Act, etc.

There are certain state specific regulations e.g. Professional Tax and

the Shop and Establishment Act which prevail in Indian states like Karnataka, Maharashtra, Tamil Nadu etc.

This is a summary of Compliances in India, Outsource Compliance is a viable solution - reach out to us.